An 1.8% increase in total household debt, up $226 billion to reach $12.58 trillion in the 4th quarter of 2016, spells bad news for the long term recovery of the US economy.

- 13k of consumer debt per person in the United States, rising 1.8% in 2016.

- Spiraling student loan and car debt fueling the rise, while housing debt remains stable.

- Pre-2008 crash levels spur worries about another financial meltdown.

Swimming Against The Current

A report by the Federal Reserve Bank’s Center for Microeconomic Data paints a worrying picture of the rising consumer debts accumulated by US citizens in 2016 and one that carries severe warnings for the future prospects of an economy relying on spending of a population drowning in credit card, automobile and student repayment schemes.

By loading the tweet, you agree to Twitter’s privacy policy.

Learn more

FRB’s research generated a few eye-catching statistics…

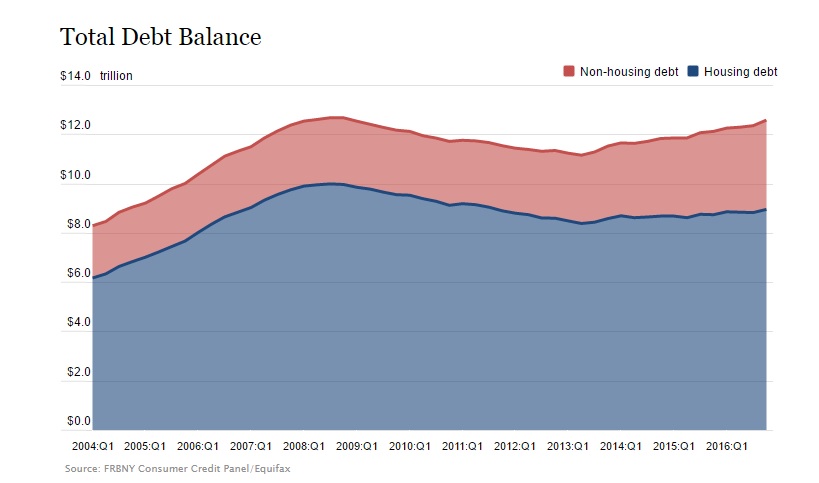

- Aggregate household debt balances grew by 1.8% in the fourth quarter of 2016, with total household indebtedness standing at $12.58 trillion, a $226 billion increase from the third quarter of 2016.

- Balances on home equity lines of credit remained mostly flat, rising $1 billion to $473 billion, while mortgage balances amounted to $8.48 trillion, rising $130 billion from the 3rd quarter of 2016.

- Non-housing debt balances rose in the 4th quarter. Vehicle financing loans rose $22 billion, with increases of $32 billion in credit cards and $31 billion in student loans fueling the rise in overall debt levels.

… but what do these numbers mean in real terms and how are economic trends impacting 320 million Americans?

A House To Call Your Own?

Interestingly, mortgages and credit card debt are actually lower than the 2008 peak as the young American workforce becomes a generation of renters.

Both the 2008 housing collapse and an aging population have motivated more people to rent, driving down mortgage debt.

The trend could well continue if an aging population stays in their home, continuing to lower the outstanding mortgage, while banks continue to require more money upfront for financing schemes.

Paying For School

Much more concerning to the future stability of the US and world economy is the increase in debt driven by higher cost student loans and car loans specifically.

What factors have contributed to those student loans being as high as they are? Are they low enough interest that people are keeping them longer?

By loading the tweet, you agree to Twitter’s privacy policy.

Learn more

More people are going to college than ever before which naturally means there will be more student loan debt.

In an age where a degree is often a necessity for even entry-level employment, colleges are charging more and increasing student debt levels to new highs.

A side effect of the 2008 housing crash saw more people go to college to retrain and skill up as jobs became less numerous and harder to get.

As for car loan debt, cars are simply getting more expensive and the loan terms are longer, often pushing buyers into 5-7 year repayment schemes that expand the scope of debt repayments.

Will Any Bubbles Burst This Time?

$4.1 trillion of economic activity was taken from our future to spend on our past – attempting to spur economic growth in a plan that will eventually stall as people reach their limit and consumer spending drops.

By loading the tweet, you agree to Twitter’s privacy policy.

Learn more

Its actually bit worse because of interest. The money that would have gone to a variety of businesses for goods and services and feeding back in to both the economy and the banks has been removed as the cost of doing something yesterday instead of today.

40 years of wage stagnation and rising costs in education, medical and housing mean that maintaining a middle class lifestyle in modern America requires debt, and an increasing amount of it.

However, this does not necessarily mean that an incoming market crash on the levels of 2008, the dotcom bubble or even the Wall Street crash is likely to occur in the next few years.

It is possible, certainly, but a more likely scenario will be a long-lasting slowdown of the economy.

In short, people are in debt for longer. The long term effects on consumer spending will likely decide the future of the US economy and the direction of financial strategy for quite some time.

Photo credit: Stefan Fussan/flickr